Many first-time homebuyers are in the early stages of their careers and will go through an exciting yet stressful journey that involves learning, financial planning, and emotional investment as they transition from being renters or living with family to becoming homeowners.

With the current upswing in mortgage rates brought by the upward trend in base rates, is this a good time to buy a house?

Why homeownership is a wise decision for first time buyers

The housing market ebbs and flows, but there's one underlying truth: homeownership is always a stable and secure thing to do.

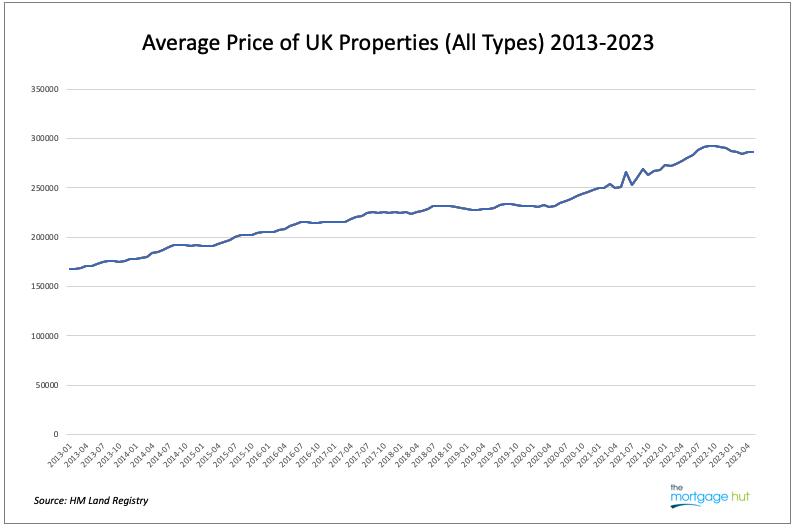

The UK real estate has historically shown appreciation over the long term. While the housing market might experience fluctuations in the short run, property values tend to rise over time as seen in the chart below that shows a 10-year average price trend of properties in the UK. The appreciation provides homeowners with potential gains in equity, contributing to their overall wealth over the long term.

Even though house prices have witnessed a dip recently, the scale of the decrease is anticipated to be modest. Historically speaking, house prices do not vary dramatically, with most economists predicting a variation of merely 10% to 12% from the peak prices.

In addition, even with a 10% drop in house prices, they are still significantly higher than pre-Covid levels. This historical trajectory indicates resilience in the real property market, making it a reliable investment option.

Homeownership also offers stability in housing costs over the long term. For instance, when you secure a fixed-rate mortgage, your monthly mortgage payments remain constant throughout the life of the loan.

Having a fixed mortgage payment therefore provides predictability in your housing expenses, making it easier to budget and plan for other financial goals. This contrasts with renting, where landlords can increase rent prices annually or as their financial needs change.

Finally, homeowners can confidently plan their long-term finances with the assurance that their mortgage payments won't change, allowing them to allocate funds to other important areas of their lives, such as savings, investments, and education.

Buy a house or continue renting?

Renters are often at the mercy of landlords' decisions regarding rent adjustments. On the other hand, homeownership frees you from the worry of sudden and unpredictable rent hikes, providing a stable living situation.

Unlike renting, homeownership allows you to gradually accumulate equity through your mortgage payments, which represents ownership stake in your home. While this isn't directly linked to your ongoing housing expenses, the equity you build serves as a valuable asset that can appreciate over time.

This equity can be tapped into through options like refinancing or home equity loans, providing a potential source of funds for important future expenditures such as education, home improvements, or unexpected financial challenges.

Mortgage payments are often comparable to or even lower than rent payments in certain areas, and you're building equity with each payment.

Additionally, owning a home offers potential tax advantages and the opportunity to customise your living environment to your preferences.

While there are upfront costs and responsibilities associated with homeownership, the financial and emotional rewards, along with the potential for future financial flexibility through accumulated equity, make buying a house a compelling option for many individuals seeking stability and long-term investment.

What support do I get when buying a house?

The UK has plenty of support programs to assist potential homebuyers, especially those trying to purchase for the first time.

For instance, the First Homes Programme in England is a government initiative designed to assist first-time homebuyers in purchasing a property not more than £420,000 in London or £250,000 anywhere else in England, after the discount of 30% to 50% of the market value has been applied.

The Key Worker Mortgage Scheme, on the other hand, addresses the challenge of high housing costs in many parts of the UK, which can make it difficult for key workers to live in the areas where they work. Through this program, key workers may qualify for housing options that are priced below the market rate, making it more feasible for them to live close to their workplaces.

Some schemes also offer shared ownership opportunities, allowing workers to purchase a portion of a property and pay rent on the remainder, reducing the upfront cost of buying a home. In some cases, key workers may be given priority access to certain housing developments or rental properties in high-demand areas.

For other affordable home ownership schemes, you may refer to the government's official page.

Interested in buying a home?

Whether you're a first-time homebuyer with limited knowledge and experience in the property market, or someone planning to remortgage your home, The Mortgage Hut has dedicated professionals ready to guide you toward the most suitable mortgage choice based on your financial profile.

Reach out to a knowledgeable advisor today by dialling 02380 980304. You can also reach us via email at info@themortgagehut.net or secure your spot by scheduling an appointment through our contact form. You may also refer your friends to us so we can help them make the right mortgage option today.